Ditch The 9 To 5 - Unleashing Financial Independence Secrets

Explore the path to financial independence with expert insights and practical tips. Discover strategies for saving, investing, and achieving financial freedom.

Author:James PierceReviewer:Camilo WoodJan 02, 202414 Shares14.2K Views

Achieving financial independenceis a transformative journey that goes beyond mere monetary goals. It's about gaining control over your financial destiny, allowing you to live life on your terms.

As you embark on this path, you'll discover the power of smart budgeting, strategic investments, and the importance of cultivating a mindset focused on long-term wealth. Whether you're aiming for early retirement, entrepreneurial ventures, or simply seeking peace of mind, the pursuit of Financial Independence empowers you to make choices aligned with your values and aspirations.

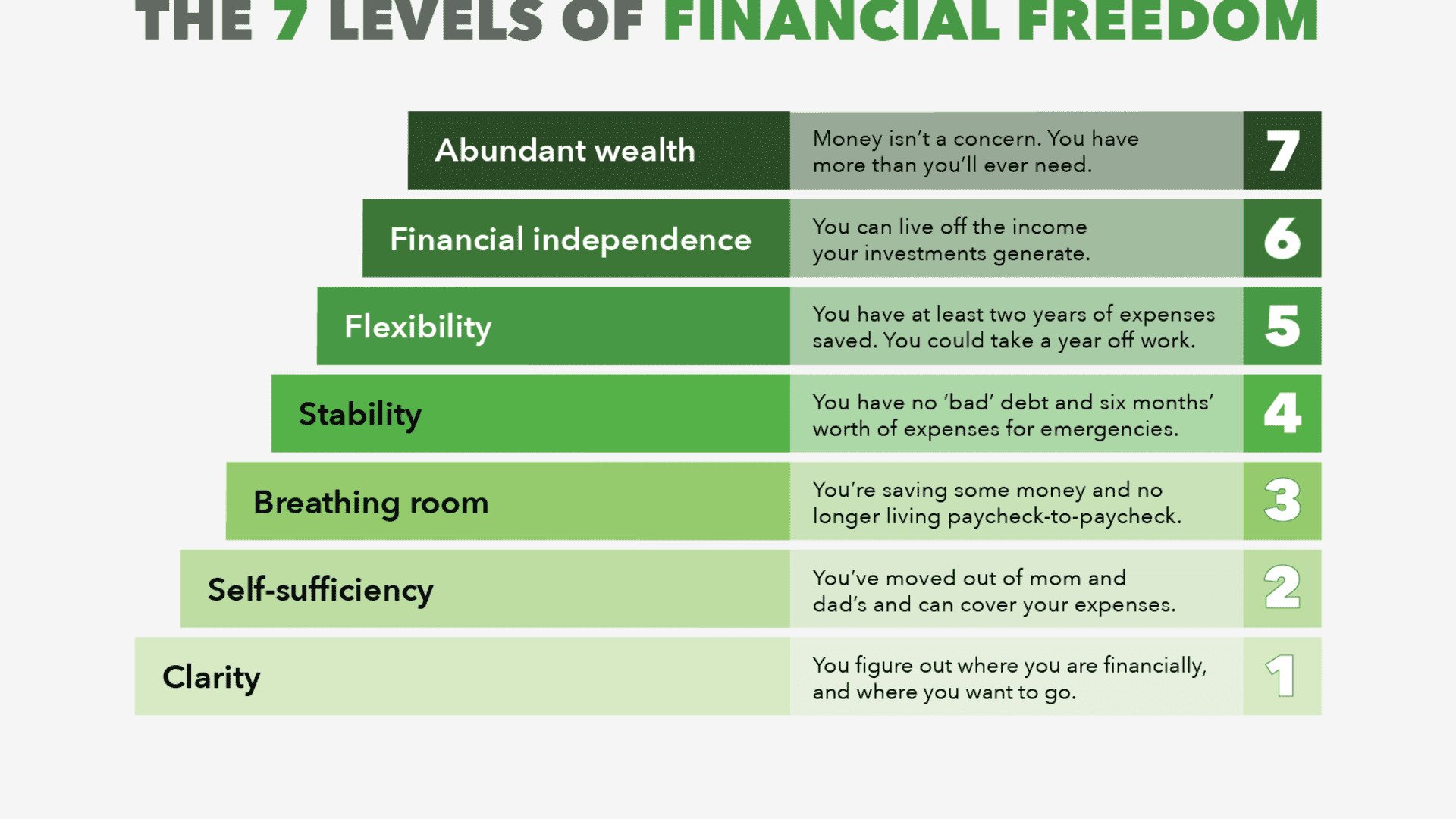

What Does Financially Independent Mean?

Financial independence is a state of financial well-being where an individual or household possesses sufficient assets and resources to sustain their chosen lifestyle without relying on traditional employment for income. This concept transcends mere wealth accumulation; it embodies the freedom to make choices aligned with personal values, aspirations, and life goals.

At its core, financial independence implies the ability to cover living expenses, handle emergencies, and pursue opportunities without being constrained by financial limitations.

Time Is Money

Time is a valuable commodity. Your money can be used to improve your quality of life today, whatever that means to you, or to buy more free time in the future to do anything you desire.

Most people make purchases using money they earned, so it's simple to calculate how many hours of work were required to afford it. Assume you earn $40 per hour and work 2,000 hours per year. You spend $40,000 on an automobile. That is about half of your total working hours for the year. All things being equal, you might have preferred to spend that time and money on something else.

It's easy to get caught up in the enthusiasm of new purchases and experiences. To avoid this, attempt to determine your core beliefs and keep an eye out for spending possibilities that correspond with your long-term objectives.

When your spending and values are out of sync, bringing them together may be one approach to spend more consciously. Making fewer unneeded purchases may allow you to save money for something you appreciate even more.

Spending less and saving more today isn't a chore if your long-term aim is to be financially independent; it's a choice that supports your future plans to take control of your life and time.

Financial Security Can Be An Advantage Of Pursuing Financial Independence For Women

Achieving financial security is creating a buffer around your finances in order to avoid a worst-case scenario, such as losing your job or being unable to work due to a catastrophic sickness or injury. Fidelity recommends saving three to six months' worth of essential costs for an emergency.

Losing a job may be an inconvenience or a heartbreak for the financially independent, but it is not a danger to their ability to maintain their lifestyle.

The Option To Accept Or Decline

Financial independence provides you with possibilities. Saying yes could be an option. If you've always wanted to explore the world for a year, you might be able to accomplish it. If family members require assistance, you may have the time, energy, and financial resources to assist.

The ability to say no to something you don't want is also strong. When money isn't the only thing holding you back, you may feel liberated to leave harmful relationships whenever you're ready.

Independence

Some people believe that waking up when they want, choosing their daily activities, and living where they want are the most valuable things money can buy. It frequently requires a sacrifice, such as foregoing a more luxurious living in order to forge their own route in life.

Ways To Acheive Financial Independence

Trouble happens to almost everyone, but these behaviors can help you get back on track.

Establish Life Objectives

What does financial independence mean to you? Everyone wants it in general, but that's an overly broad goal. You must be specific about the quantities and deadlines. The more explicit your goals, the more likely you are to achieve them.

Make a list of the following three goals -

- What your way of life necessitates?

- How much money should you have in your bank account to make that happen?

- What is the age limit for saving that amount?

Then, working backward from your deadline age to your current age, set financial mileposts at regular intervals between the two dates. Make a detailed note of all amounts and timeframes, and place the goal sheet at the front of your financial binder.

Develop A Monthly Budget

Making and sticking to a monthly home budget is the best method to ensure that all bills are paid and savings are on track. It's also a daily practice that reinforces your goals and helps you resist the urge to splurge.

Pay Off Credit Cards Immediately Full

Credit cards and other high-interest consumer loans are detrimental to wealth creation. Make a point of paying off the entire balance each month. Student loans, mortgages, and other comparable debts often have significantly lower interest rates, so repaying them is not an urgent need. However, making on-time payments on these lower-interest loans is still important, and making on-time payments will help you build a high credit rating.

Set Up Automatic Savings

First and foremost, pay yourself. Enroll in your company's retirement plan and take advantage of any matching contribution benefit, which is effectively free money. It's also a good idea to set up an automatic withdrawal into an emergency fund that may be used for unanticipated needs, as well as an automatic donation to a brokerage account or something similar.

The money for the emergency fund and the retirement fund should ideally be withdrawn from your account on the same day you receive your paycheck, so it never crosses your hands.

Remember that the suggested amount to save in an emergency fund is dependent on your specific circumstances. Also, tax-advantaged retirement plans have limitations that make it difficult to access your money if you need it right away, so that account should not be your primary emergency fund.

Begin Investing Right Away

People may doubt the idea of investing in bad stock markets, known as bear markets, yet there has historically been no better way to grow your money. Compound interest alone will grow your money tremendously, but it will take a long time to attain meaningful growth.

Remember, however, that attempting the type of stock selecting made famous by billionaires like Warren Buffett would be a mistake for everyone but experienced investors. Instead, register an online brokerage account that allows you to easily learn how to invest, build a modest portfolio, and make automatic weekly or monthly payments to it.

Keep An Eye On Your Credit Score

Your credit score is a critical figure that influences the interest rate you are offered when purchasing a new automobile or refinancing your home. It also affects the price you spend for a variety of other necessities, such as vehicle insurance and life insurance premiums.

Credit ratings are so important because someone with risky financial habits is more likely to be careless in other aspects of life, such as not taking care of their health, or even driving and drinking.

This is why it is critical to obtain a credit report at regular intervals to ensure that there are no incorrect black marks tarnishing your reputation. It may also be worthwhile to investigate a trustworthy credit monitoring service to safeguard your information.

Contract For Goods And Services

Many Americans are unwilling to bargain for products and services because they are fearful of appearing cheap. If you can overcome this phobia, you might save hundreds of dollars each year. Small firms, in particular, are willing to negotiate, so buying in bulk or establishing yourself as a regular customer can lead to substantial savings.

Maintain Your Financial Knowledge

Examine applicable tax law changes to ensure that all adjustments and deductions are maximized each year. Keep up with financial news and stock market movements, and don't be afraid to adjust your investing portfolio accordingly. Knowledge is also the best defense against con artists that prey on inexperienced investors in order to make a quick buck.

Keep Your Property In Good Condition

Property maintenance extends the life of everything from vehicles and lawnmowers to shoes and clothing. Maintenance is a fraction of the cost of replacement, thus it is an investment not to be overlooked.

Live Within Your Means

Developing a thrifty mindset involves focusing on living a good life with less—and it's easier than you think. In fact, many affluent people adopted the habit of living below their means before becoming wealthy.

Adopting a simple lifestyle is not difficult. It simply involves learning to discriminate between what you need and what you want—and then making little changes that result in large financial rewards.

Consult With A Financial Advisor

Once you've built a reasonable amount of wealth, either liquid assets (cash or anything easily converted to cash) or fixed assets (property or anything not easily converted to cash), hire a financial counselor to keep you on track.

Maintain Your Health

Proper maintenance also applies to your body, and taking exceptional care of your physical health has a huge positive impact on your financial health.

It is not difficult to invest in one's health. It entails seeing doctors and dentists on a regular basis and following medical advice for any problems you encounter. Many medical disorders can be helped, or even prevented, by making simple lifestyle changes like increasing physical activity and eating a better diet.

Poor health maintenance, on the other hand, has both immediate and long-term financial effects. Some companies put a limit on sick days, which results in a loss of income after paid days are depleted. Obesity and other dietary disorders raise insurance rates, and bad health may compel you to retire early and live on a lesser monthly income for the rest of your life.

Benefits Of Financial Independence

You Can Live And Work On Your Own Terms

If your passive income exceeds your outgoings, you have the freedom to choose how you work, who you work with, and how long you work; you are not at the mercy of employers or employment contracts. This provides you more negotiating power for your future position. If pay is unimportant, you can have more of what is important to you. It could be working hours, vacation time, autonomy, or project selection.

When we are no longer restrained by the 'golden handcuffs' of a wage, the job market becomes much more fascinating. If your assets are paying for your lifestyle, you may choose to start a business or invest in a personal project that is not related to a regular salaried job.

Increased Financial Stability

Job security is becoming increasingly illusory. Zero-hour contracts are becoming more common, fundamentally altering how businesses run. A job for life does not exist as it once did.

Being financially independent puts you in a better position to avoid being at the mercy of these influences. When you have financial independence, you can choose occupations that suit your risk tolerance rather than being reliant on a wage.

Unemployment Benefits

With savings and investments in place, you don't have to rely on modest unemployment compensation that just cover the essential requirements; you may continue to enjoy a nice lifestyle.

You should not stop working because you have gained financial freedom. You may desire to expand your fortune, enhance your standard of living, or save for your children. However, if you or your partner lose your job, you can rest assured that your lifestyle will be safeguarded and you will not have to make any changes.

Extra Investment Potential

Your assets and investments may generate additional income that you would not have received otherwise. Consider it a bonus on top of your regular paycheck that you get to pay yourself. Money gained outside of a labor/salary transaction is frequently identified by our clients as one of the top benefits of financial freedom.

And the sooner you attain financial independence, the sooner you can start building your personal wealth. Compound interest is frequently referred to as the world's eighth wonder.

When you no longer need to withdraw the profits from your investments and instead reinvest them, compound interest kicks in. In the example below you can see the difference being able to invest over a lengthy period makes when the interest compounds. The basic investment in both cases is €72,000, however the difference in returns is €35,000.

If you start saving €300 a month today and continue to do so for the next 20 years, you would have saved €72,000. If you put this money into a savings account that earns 5% interest per year, you will have saved €124,989 after 20 years.

If you delay saving for another 8 years, you will need to invest €500 per month. With the increased premium, you will save €72,000 in 12 years and your balance will be €90,015 with the same 5% rate of interest.

Retirement At A Young Age

The truth of government-funded retirement is that the payouts are rarely sufficient to maintain the lifestyle that most of us envision for our golden years. In addition, with our ever-increasing life expectancy, the majority of countries are delaying retirement age.

Those who want to retire early, whether at 45 or 60, must have a money stream that will sustain their lifestyles well beyond the normal life expectancy. This percentage can vary depending on your circumstances, but you can learn more about the 4% rule and how much to save for retirement here.

Mind-body Harmony

You will have more flexibility if your passive income exceeds your minimum expenses. Removing the worry of a job-related income is extremely liberating. As previously said, many clients continue to work and build their personal wealth. They do it, however, without the stress of needing to get the next promotion for a pay raise.

The less stress we have in our lives, the happier we will be. Money problems are frequently considered as one of the most stressful aspects of our life, and they are frequently the source of family strife. Financial independence affords choice, which is why so many of us seek for it.

Financial Independence - FAQs

What Role Does Budgeting Play In Achieving Financial Independence?

Budgeting is a fundamental aspect of Financial Independence. Creating and sticking to a budget helps control spending, increases savings, and ensures that you allocate resources towards your financial goals.

Can Entrepreneurship Contribute To Financial Independence?

Absolutely. Entrepreneurship provides opportunities to generate additional income streams and build wealth. Starting a business aligned with your skills and passions can significantly impact your journey toward Financial Independence.

How Does Financial Independence Relate To Early Retirement?

Financial Independence often precedes early retirement. Achieving financial freedom allows individuals to retire early if they choose, giving them the flexibility to pursue other interests and activities.

Is Financial Independence Only About Money, Or Does It Involve Lifestyle Choices As Well?

Financial Independence extends beyond finances; it encompasses lifestyle choices aligned with personal values. It's about having the freedom to design a life that brings fulfillment and happiness.

Can Debt Hinder The Path To Financial Independence?

Yes, excessive debt can impede progress toward Financial Independence. It's crucial to manage and reduce debt while focusing on building assets and increasing income.

Are There Risks Associated With The Pursuit Of Financial Independence?

Like any financial goal, there are risks. Market fluctuations, unexpected expenses, or changes in personal circumstances can impact progress. Diversification and contingency planning help mitigate these risks.

Final Words

The quest for financial independence is not just about accumulating wealth; it's a holistic approach to designing a life that reflects your dreams. By making informed financial decisions, cultivating a savings habit, and investing wisely, you lay the groundwork for a future marked by autonomy and security.

As you reach milestones on this journey, remember that true financial freedom is not just a destination; it's a continuous evolution. Embrace the lessons learned, adapt to changing circumstances, and relish the freedom to shape your destiny. Financial independence is not merely a goal; it's a lifestyle that affords you the flexibility to live life on your own terms.

James Pierce

Author

Camilo Wood

Reviewer

Latest Articles

Popular Articles